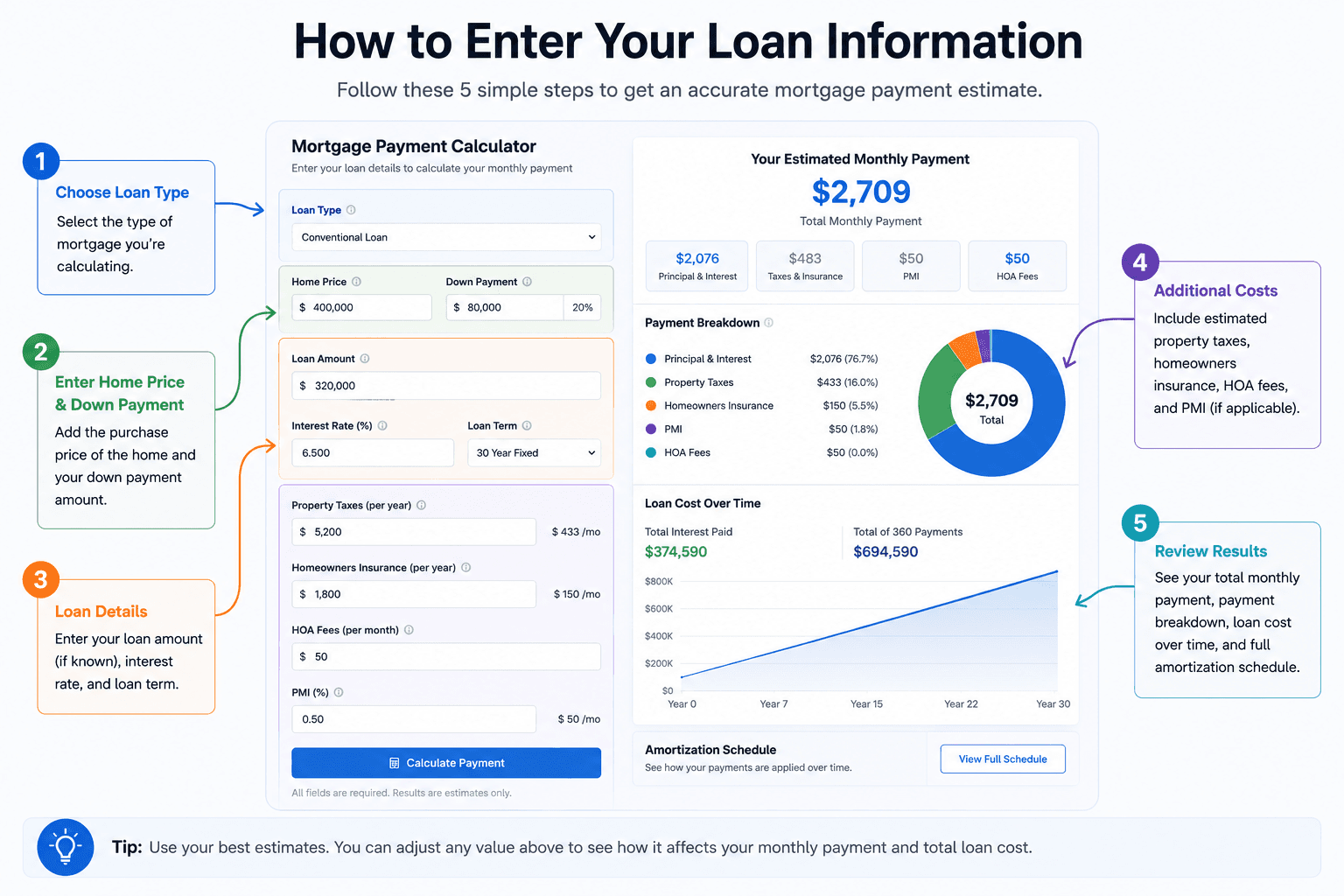

Mortgage Payment Calculator: Estimate Your Monthly Payment

Enter your loan details to calculate your monthly payment.

Results update automatically as you change any value.

Payment Breakdown

First payment estimateLoan Cost Over Time

What These Results Mean

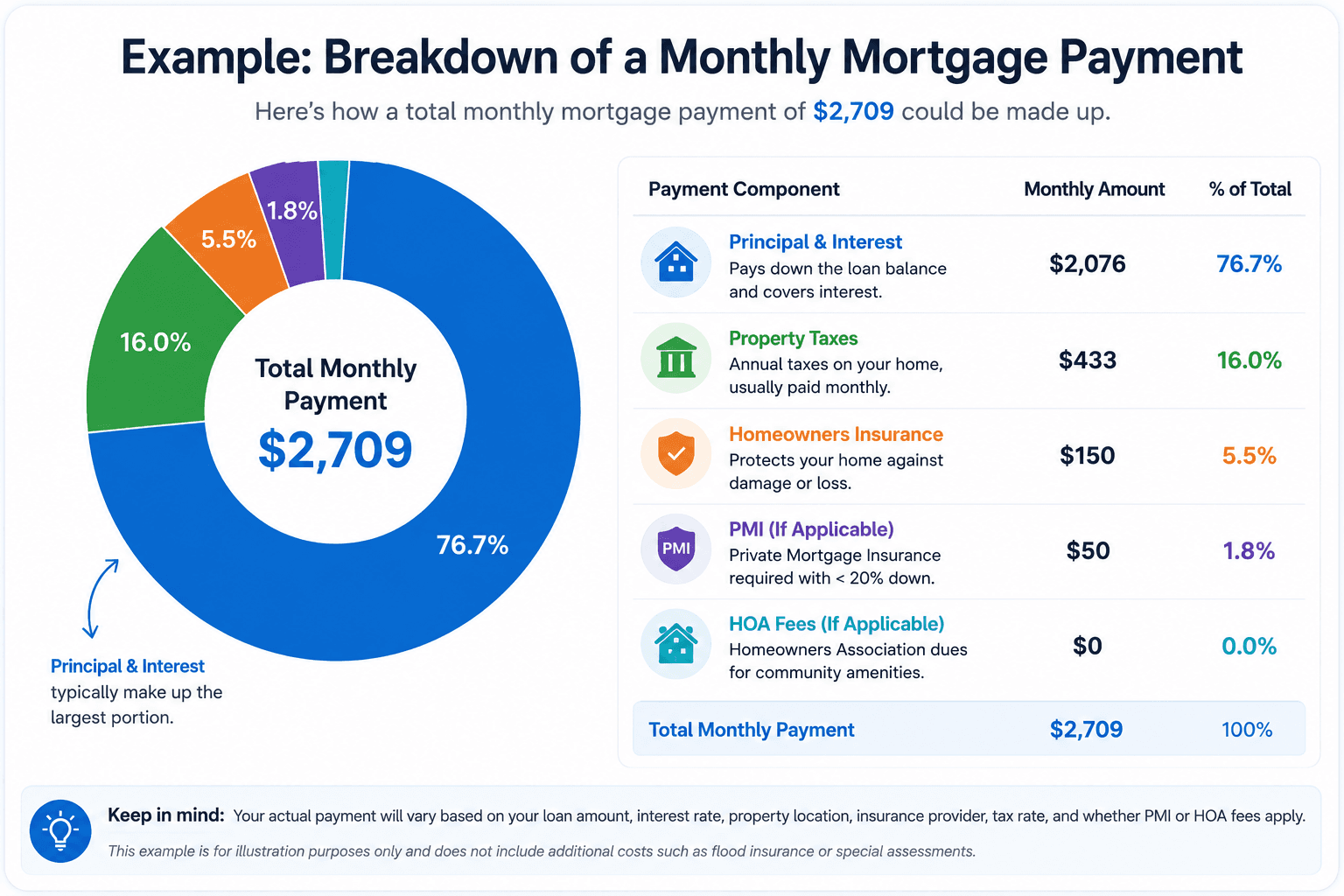

With a 30-year conventional loan of $320,000.00 at 6.750%, your estimated first-month housing payment is $2,708.85. The loan is projected to be paid off in Aug 2056, assuming the entered rate and payment schedule remain unchanged.

Amortization Schedule Breakdown

Expand the annual or monthly schedule to review principal, interest, housing costs, extra payments, and remaining balance.

Ready to compare this payment with real lender offers?

Review available mortgage rates and lender details in the live rate table below.

Welcome to Mortgage Payment Calculator, your trusted partner in navigating the complexities of home financing. Our easy-to-use tool allows you to accurately estimate your monthly mortgage payments, factoring in taxes, insurance, and Private Mortgage Insurance (PMI). Whether you are a first-time homebuyer or looking to refinance, understanding these components is crucial for determining affordability. With our comprehensive amortization schedule, you can visualize how your mortgage evolves over time, empowering you to make informed financial decisions confidently. Start leveraging our calculator today to take control of your home financing journey.

Brief Overview

The Mortgage Payment Calculator is a valuable tool for accurate estimation of monthly mortgage payments, incorporating essential elements like taxes, insurance, and Private Mortgage Insurance (PMI). Ideal for homebuyers and those considering refinancing, it offers insights into interest rates, loan terms, and payment structures. Users can access comprehensive amortization schedules to understand the evolution of mortgage payments over time, enabling informed financial decisions. The calculator assists in evaluating various financial scenarios, ensuring users are equipped to manage their home financing effectively, accommodating different interest rates and local tax considerations.

Key Highlights

- Mortgage Payment Calculator simplifies estimating monthly payments, including taxes, insurance, and PMI, crucial for determining home affordability.

- Taxes, insurance, and PMI significantly influence mortgage payments, affecting both immediate obligations and long-term costs.

- Understanding interest rates and how they impact monthly payments is key to managing home financing effectively.

- Access to comprehensive amortization schedules aids in visualizing loan repayment progress, offering deeper financial insights.

- Choosing between 15-year and 30-year terms involves weighing lower interest against higher monthly payments and long-term affordability.

Understanding the Basics of Mortgage Payments

Understanding the basic components of homeownership costs is essential when you're getting ready to estimate your monthly mortgage payment. A typical mortgage loan involves a diverse range of costs beyond just the principal and interest. Monthly mortgage payments generally encompass not only the borrowed amount but also the insurance and taxes. Taking costs like insurance into account can greatly affect homeowners' total monthly mortgage responsibilities. Another key aspect to consider is PMI, or private mortgage insurance, which lenders might require if your down payment is less than 20%. These elements collectively ensure you're covering more than just the loan; you're securing your home as well. When utilizing our online tools, like the Mortgage Payment Calculator, you'll have the advantage of estimating monthly mortgage payments accurately. Accurately calculating your mortgage payment empowers you with a clearer picture of what your monthly payment will be. This comprehensive understanding allows homeowners to navigate their financial commitments confidently and ensures you're ready to face fluctuating interest rates and market variables. Our tools consider each layer of your mortgage, offering insights into how insurance or taxes impact your overall costs. Whether you're a first-time homebuyer or considering a new mortgage loan, knowing these basics supports informed financial decisions and lays the groundwork for stable, sustainable homeownership costs.

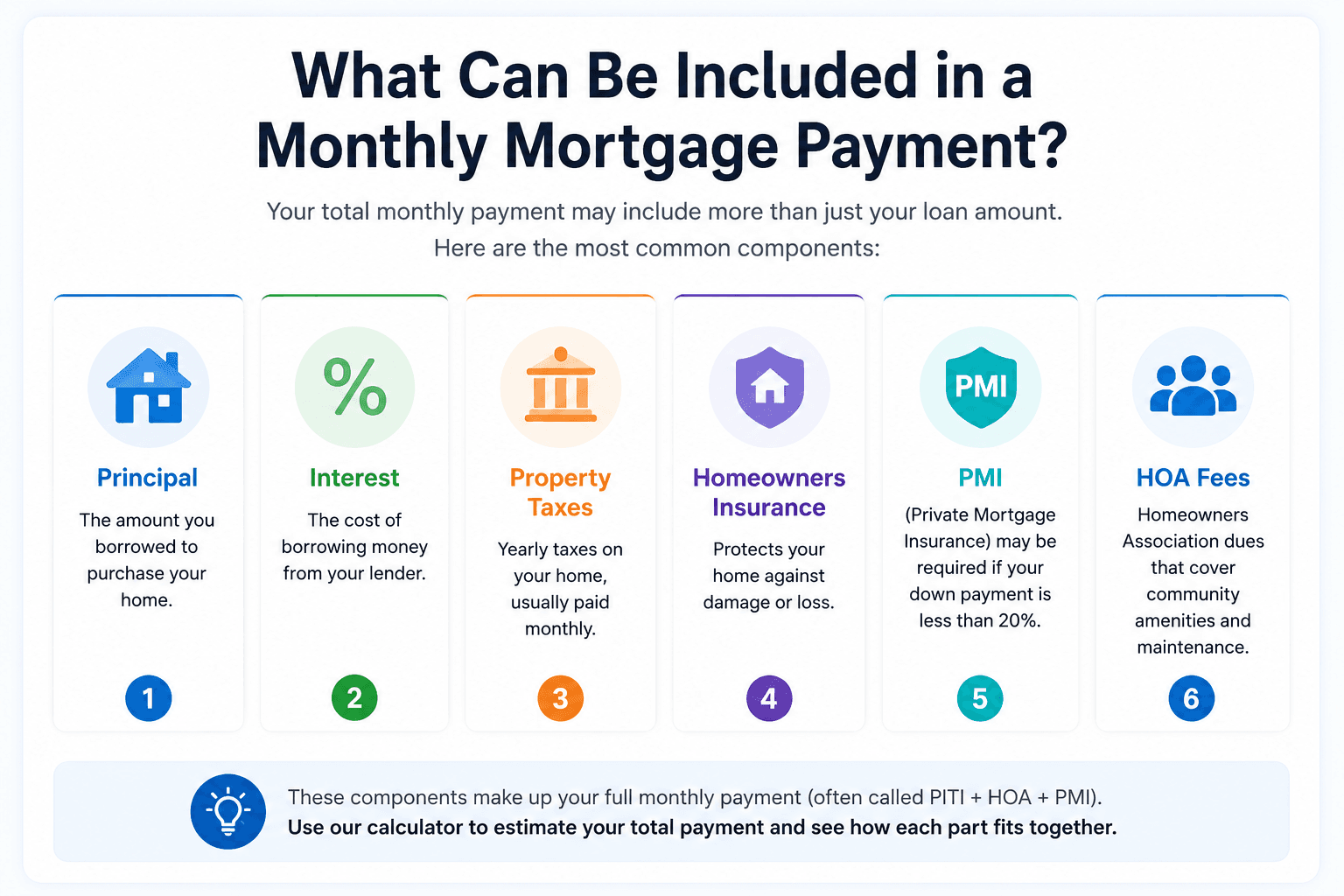

What Constitutes a Total Monthly Mortgage Payment?

When considering a monthly mortgage payment, it's crucial to understand the various components that constitute this payment amount. At the core, your monthly mortgage is composed of the principal and interest of your loan amount, this is the direct repayment of the loan. However, to accurately assess your financial commitment, you must also consider taxes, insurance, and PMI, often tied to home loans. Property taxes are a recurring expense, varying based on your property's assessed value and location. Similarly, homeowners insurance safeguards your home and is integrated into the total monthly payment. PMI, or private mortgage insurance, is typically required if your equity is less than 20%, adding an extra layer to your payment. Tools such as mortgage calculators are invaluable for calculating these elements. Understanding how each affects your overall financial picture is integral. While one might calculate a loan using just numbers, omitting taxes, insurance, and PMI can lead to an inaccurate view of affordability. Mortgage calculators can also help explore various interest rates and their impact on your payment, providing insight into equity growth over time. A comprehensive look at your amortization schedule through these calculators reaffirms the critical nature of these components in understanding your home loan. With this knowledge, borrowers can manage their finances effectively, ensuring a clear path towards property ownership and equity building.

The Role of Taxes, Insurance, and PMI

Understanding the intricacies of your mortgage payment involves more than just principal and interest. Utilizing a comprehensive mortgage payment calculator allows you to factor in essential elements such as taxes, insurance, and PMI (Private Mortgage Insurance), which are crucial for determining the true cost of homeownership. Incorporating these elements into your calculations provides a realistic view of your financial obligations. Taxes, based on your property's value, can significantly influence your monthly payment. Understanding your local tax rates ensures you’re never caught off guard by unexpected costs. Meanwhile, homeowners insurance, an indispensable component, protects your property and adds to your monthly outlay. Our calculator includes insurance estimates, enabling you to gauge your total costs accurately. PMI is another critical aspect for those with less than 20% home equity, as lenders often require this insurance to mitigate risk. It’s vital to remember that PMI can increase your monthly payment but drops off once sufficient home equity is built. A clear understanding of how these factors interplay will help you prepare more effectively for the financial responsibilities of owning a property. Utilizing our mortgage payment calculator ensures that you account for taxes, insurance, and PMI, thereby providing a transparent overview of your housing costs and positioning you to make informed financial decisions regarding your property.

How to Use the Mortgage Calculator Effectively

To accurately estimate your monthly mortgage payment, our mortgage calculator is one of the most effective tools available. When you enter the relevant information, ensure accuracy by using no more than two decimal places. This ensures the estimates you receive are precise and reliable. Start by entering the principal loan amount, interest rate, loan term, and additional costs like taxes, insurance, and PMI. These inputs provide a holistic view of your financial obligation, allowing more informed decisions. Calculators like ours incorporate these variables to facilitate comprehensive calculations, helping you gauge true affordability.

After entering the necessary data, viewing the breakdown of your estimates is crucial. The calculator offers a detailed amortization schedule, showing how each payment is allocated towards principal and interest. This insight is invaluable for planning long-term finances. Beyond immediate figures, the tool provides a forecast of annual amortization trends, empowering you with knowledge about future payment shifts based on different loan scenarios.

Finally, by testing various interest rates and loan terms, you can assess how these factors impact your monthly dues. The right combination can mean significant savings. Utilizing our mortgage calculator and the array of tools it offers enhances your understanding of mortgage dynamics, making the process of home financing more manageable and less intimidating.

Entering Your Loan Information

Entering your loan information accurately is a vital step in obtaining precise calculations using our Mortgage Payment Calculator. It's essential to provide the correct details about your loan, including the loan term, interest rate, and loan amount. Accurate inputs enable you to better estimate monthly mortgage payments, taking into account factors like taxes, insurance, and PMI. When beginning the process of entering your loan data, consider how each element impacts affordability. Whether you're venturing into home lending for the first time or leveraging home equity, these figures form the cornerstone of your financing strategy. By carefully detailing your loan specifics, you set the stage for sound home lending decisions. The Mortgage Payment Calculator makes entering information simple, guiding you through each step to bring clarity to your financial outlook. Dive into these calculations with the assurance that the tool is designed to assist with accurate home equity assessments and precise estimates of monthly mortgage payments. Lending professionals frequently recommend thoughtfully approaching these initial steps to ensure every aspect of the loan details is perfectly aligned with your home lending goals. Thoughtful entering of information, in tandem with sound financial advice, transforms complex home equity and loan data into manageable steps towards home ownership.

Viewing Your Mortgage Repayment Summary

When you've entered your loan details, it's time to delve into the crucial aspect of viewing your mortgage repayment summary. This summary delivers insights into how your monthly mortgage payments are structured over the life of your mortgage loan. Effective use of mortgage calculators can aid in visualizing how each monthly payment impacts the overall repayment of the loan. Your mortgage payment summary not only gives an overarching view of your payments but also helps estimate your monthly mortgage payment in advance, thus offering a clearer picture of what to expect. With this summary, you gain a profound understanding of your loan's components, which include principal and interest, as well as other elements like taxes, insurance, and private mortgage insurance (PMI). The detailed breakdown allows you to anticipate future expenses and manage your finances efficiently. The importance of accurately identifying your repayment schedule cannot be overstated, as it impacts both short-term budgeting and long-term financial planning. As part of this summary, you will also encounter data that aids in tracking loan balances, ensuring you maintain awareness of your financial obligations throughout the loan's duration. Ultimately, the summary is a powerful tool in your home financing journey, furnishing you with essential insights for smart financial decisions.

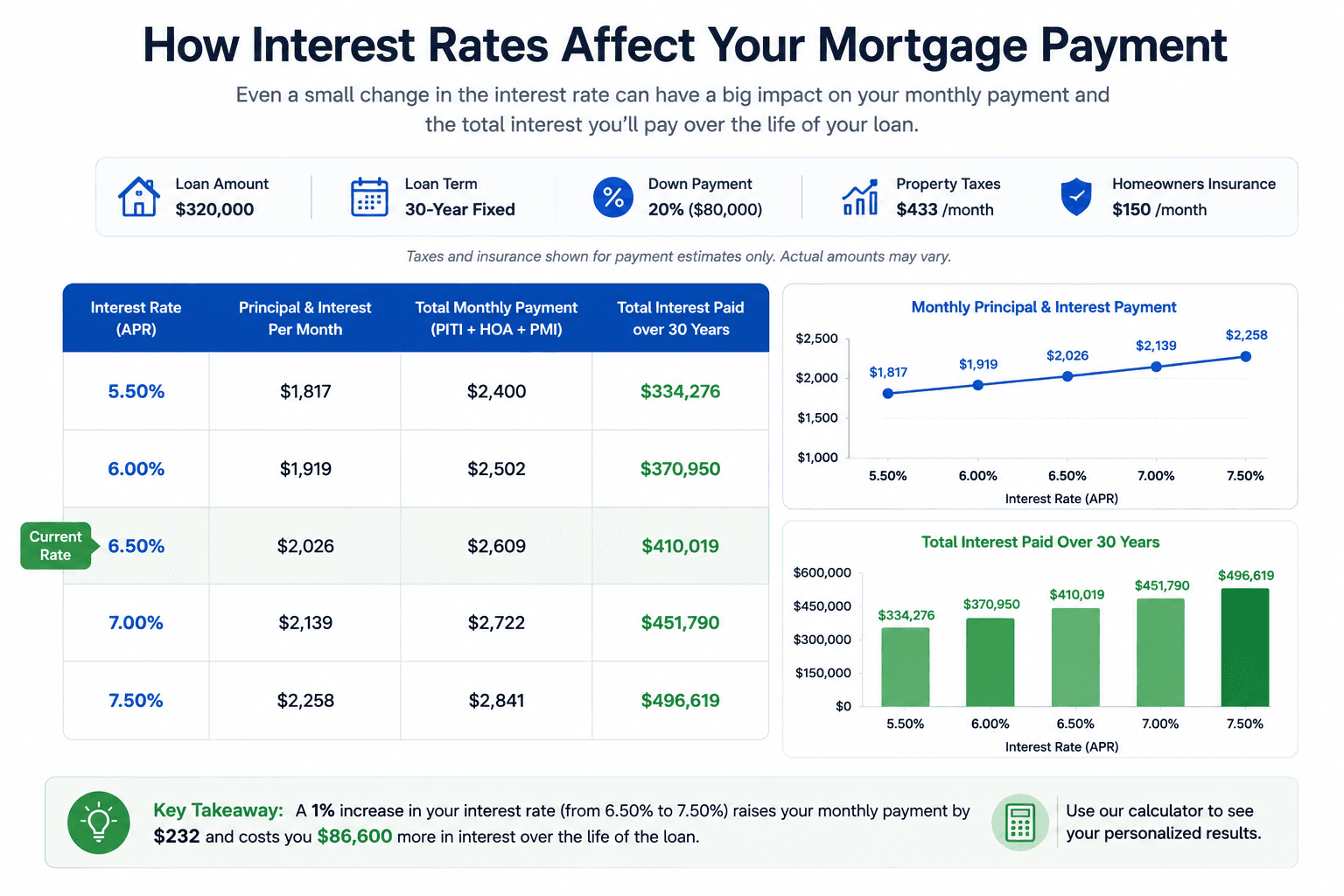

Exploring Interest Rates and Their Impact on Cost

Interest rates play a pivotal role in determining the overall cost of your mortgage. An interest rate can significantly impact your monthly payments and the total amount paid over the life of the loan. When you use a mortgage payment calculator, understanding how different rates affect your monthly payment is essential. The interest rate affects not only the immediate payment but also the long-term affordability of homeownership. By analyzing various interest rates, you can identify options that align with your financial capacity. With fluctuating rates, borrowers must stay informed about current trends, as even small changes in the interest rate can result in substantial differences in monthly costs. By inputting different rates into our mortgage payment calculator, you can assess potential future scenarios and their implications on your budget. Understanding interest is crucial when considering refinancing, as a lower interest rate can reduce monthly payments or shorten the loan term. It’s essential to remember that mortgage rates vary based on economic conditions, your credit score, and loan type. Therefore, evaluating varying interest rates through our calculator helps prepare you for making well-informed financial decisions. Effectively managing the rates you obtain ensures you remain within your desired budget while pursuing your homeownership goals. With interest at the forefront, strategically utilizing a mortgage calculator provides clarity in your financing journey.

How Interest Rates Affect Your Monthly Payment

Interest rates are a crucial factor in determining your monthly mortgage payment. When interest rates rise, the dollar amount you'll need to meet your monthly payments generally increases. Conversely, when interest rates fall, your monthly payment amount tends to decrease, providing potential savings on home financing costs. It's important to note that even a small change in interest rate can significantly affect the total interest paid over your mortgage's life, impacting the final payment amount. The cost of your loan depends on these rates and affects your financial planning. By proactively managing your interest, you can estimate your monthly mortgage payment more accurately using our Mortgage Payment Calculator. By evaluating different interest scenarios, our calculator helps you understand the effect of various interest rates on your financial bottom line. To get a precise estimate of your monthly payment, inputting different interest rates into the calculator allows you to see how each rate adjustment affects your monthly mortgage cost. It's essential for all borrowers to explore various interest rates to determine how they will impact their total monthly payments and, ultimately, their affordability. Equip yourself with this understanding to make informed decisions. Whether you're a first-time buyer or refinancing an existing mortgage, understanding how interest rates affect your monthly payment is critical in planning your financial future.

Choosing the Right Interest Rate for You

When it comes to home lending, selecting the right interest rate is crucial for both immediate savings and building long-term equity. Understanding how interest rates impact your monthly mortgage payment can help you make informed decisions. Higher interest rates mean increased monthly payments and less savings over time, while lower rates could enhance your financial freedom and boost your savings. But, how do you determine the right rate for you? Start by researching current rates and trends in the market. Interest rate fluctuations can significantly affect your overall costs, so it's important to act when rates are favorable. Remember, the rate you choose will have a direct influence on your monthly payments and the overall interest accrued, impacting your lifetime mortgage cost. Fixed-rate mortgages offer stability with predictable payments, whereas adjustable-rate mortgages provide initial savings with variable future rates. Evaluating your financial goals, considering your long-term savings strategies, and understanding how equity accumulation ties into the rate you choose are all vital steps. Securing the right interest rate can lead to substantial savings and expedite equity growth, making it an essential factor in home lending decisions.

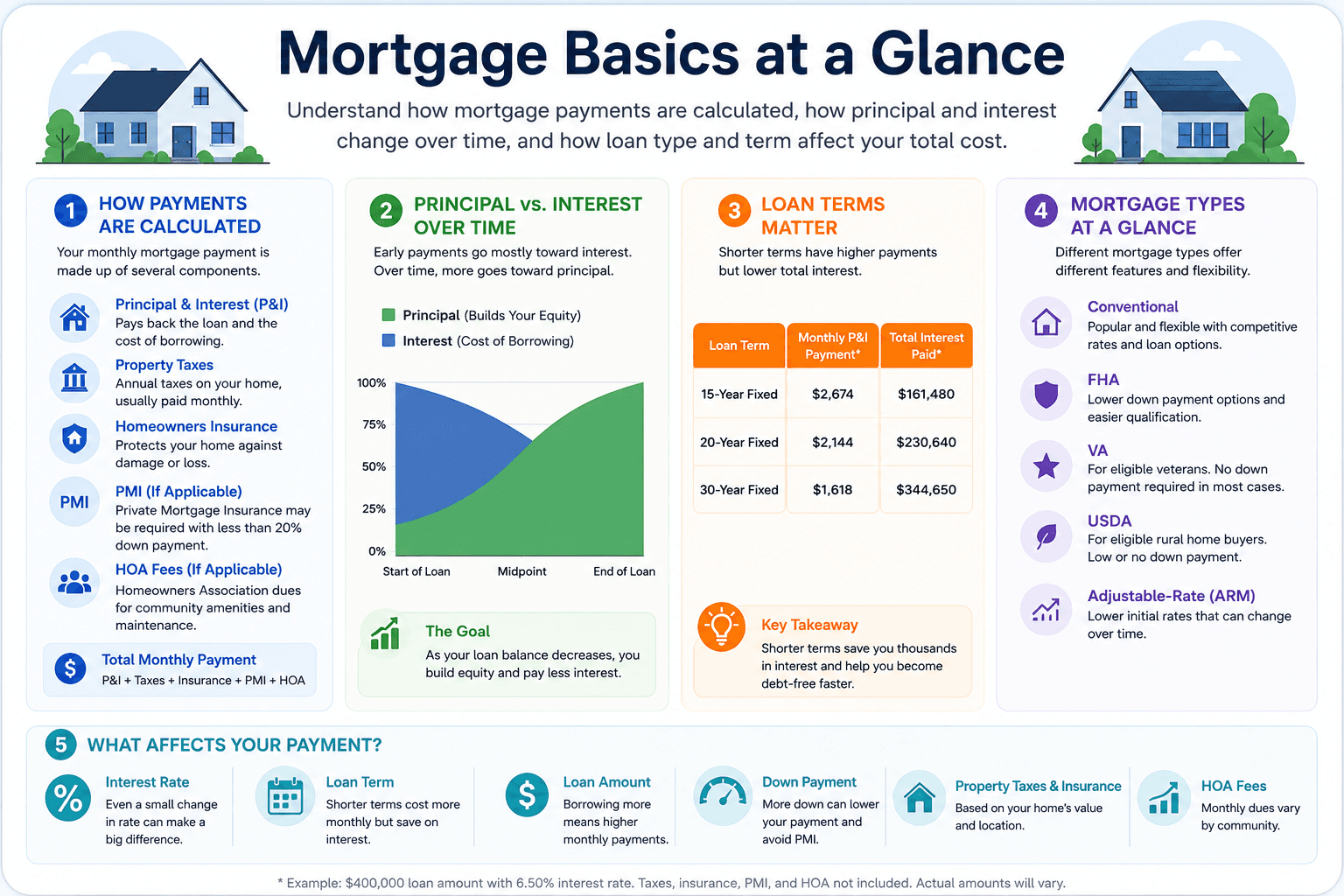

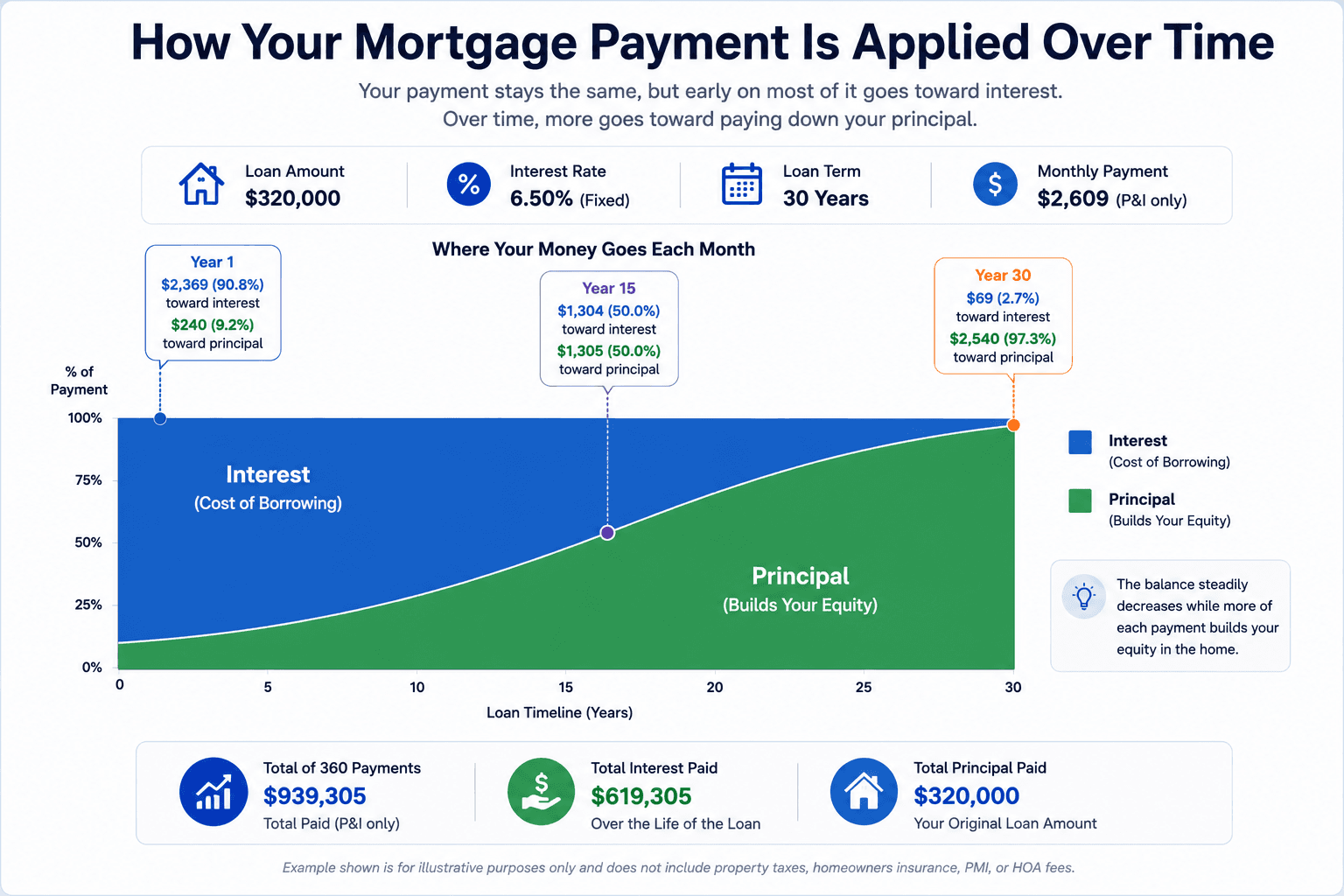

Analyzing Your Amortization Schedule

Understanding the intricacies of your amortization schedule is crucial when it comes to handling your mortgage effectively. By analyzing the amortization plan provided by our mortgage calculators, you can gain valuable insights into how your home loans will be distributed over time. A well-detailed mortgage calculator provides a comprehensive view, showcasing how much of your early payments go towards interest as opposed to equity, an essential aspect to ponder for anyone engaged in home lending decisions. With good planning, you’ll see how gradually, your repayments start contributing more towards the principal. This calculations approach enables you to strategize your payment schedule more effectively, especially if you're considering refinancing or tapping into home equity. Moreover, the mortgage calculator will reveal the impact of items such as taxes, insurance, and PMI on the overall cost, allowing you to make informed choices. A periodic review of your mortgage terms and repayment situations helps you navigate lending options that align with your financial goals. Whether you’re new to home loans or are considering different lending alternatives, analyzing your amortization schedule empowers you on your financial journey, making those complex calculations and payments much more manageable in the long run.

Monthly Amortization Breakdown

Understanding the monthly amortization breakdown is essential when navigating mortgage payments. At the core of mortgage calculators, the monthly breakdown provides a clear view of your payment schedule, ensuring you comprehend the intricacies of your loan. By using a reliable mortgage calculator, like the one offered by Mortgage Payment Calculator, you can easily view the dollar amount allocated to principal repayment and interest payments. This insight helps in understanding how much of each monthly payment is applied toward reducing the loan balance and how much goes toward interest. Calculating the payment amount, while considering taxes, insurance, and PMI, gives you a comprehensive view of the total monthly obligation. Your schedule will illuminate repayment progression, highlighting the shift of dollar allocations over time. Consistently entering your loan information into mortgage calculators provides accuracy in predicting future repayments. As you explore your mortgage payments in detail, you'll see the impact of different interest rates on your payment amount. By analyzing monthly schedules, you can make informed decisions about your home loans. A thorough understanding of the amortization breakdown aids in planning your future financial health and ensures you’re equipped to manage your mortgage effectively. Therefore, utilizing calculators is an invaluable tool for anyone looking to dissect the dollar dynamics of their loan.

Understanding Annual Amortization Trends

Understanding annual amortization trends is essential for borrowers aiming to estimate monthly mortgage payments accurately. Using our mortgage calculators, you can estimate your monthly mortgage payment by examining how amortization impacts your loan over time. Mortgage payments consist of principal and interest rates that change due to amortization and can significantly affect your savings. Observing these trends allows you to strategize around savings opportunities, enabling better planning as interest rates fluctuate. Our easy-to-use mortgage calculator includes amortization schedules, illustrating how your mortgage payments are allocated to interest and principal throughout the year. This insight into amortization can help you choose loans that align with your financial goals while managing costs effectively.

Additionally, observing annual trends in home equity assists in predicting potential savings and loan affordability over the term of your loan. By learning how various interest rates and loan structures influence annual amortization, you’re better equipped to make informed decisions about refinancing and mortgage adjustments. Knowledge of amortization patterns aids in understanding the complexities of mortgage payments, resulting in a more accurate estimation of costs. Ultimately, comprehending amortization trends empowers you with the knowledge to utilize our mortgage calculators effectively, assuring comprehensive financial planning.

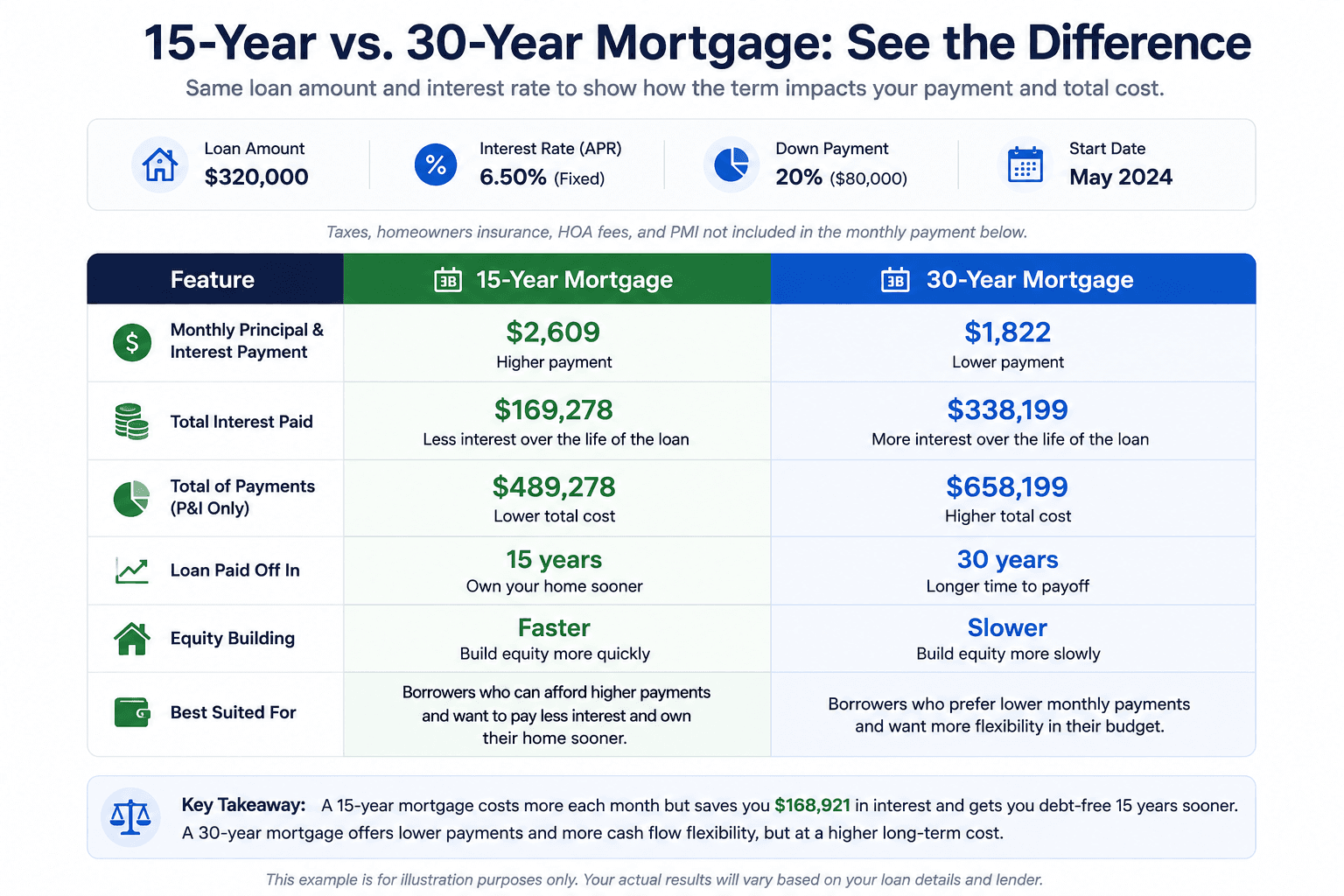

Deciding Between a 15-Year and 30-Year Term

When deciding between a 15-year and 30-year loan term, it’s essential to consider several factors affecting mortgage payments. A 15-year loan will typically offer lower interest rates compared to a 30-year term, which means you’ll pay less overall mortgage interest throughout the life of the loan. However, mortgage payments will be higher than with a 30-year term. It's crucial to determine if you can comfortably manage the larger monthly mortgage payment that comes with a shorter loan term.

Choosing the right loan term also impacts your home equity accumulation. A 15-year mortgage allows you to build equity faster and can be ideal if your goal is to own your home outright more quickly. On the other hand, a 30-year loan offers more flexibility in your budgeting, leaving room for other financial priorities. When considering home loans, look at how each loan term affects total costs, interest paid, and equity gains.

The decision between years of financing shouldn’t be made lightly, as it shapes the financial landscape of your homeownership. Use the Mortgage Payment Calculator on our website to see how different loan terms impact your mortgage payment. By comparing options, you’ll make an informed choice that aligns with your long-term financial goals. Remember, years of thoughtful planning and calculations will yield the best approach for managing home loans.

Factors to Consider When Choosing Your Loan Term

When choosing your loan term, it's crucial to consider several factors that can impact your long-term financial plans. The length of the loan term can significantly affect your mortgage payments and overall costs. A longer loan term typically results in lower monthly payments but can increase the total interest paid over time. Conversely, a shorter term may lead to higher monthly payments, yet reduces the total interest paid in the long run. Interest rates play a vital role in determining the payment amount. It’s wise to carefully evaluate mortgage rates and choose a loan term that aligns with your budget and goals. Our Mortgage Payment Calculator can assist you in doing just that by helping you analyze your mortgage calculation and understand how different terms affect your payment amount. Don't forget to factor in other costs like taxes, insurance, and PMI, which can influence your monthly obligations. Additionally, a comprehensive appraisal of your mortgage repayment summary and amortization schedule can offer insights into how a loan term impacts your finances. Whether you're looking into a 15-year or 30-year loan, take into account these various considerations along with your interest rate options. By exploring these elements, you can make informed home lending decisions that cater to your financial situation.

Mastering your mortgage payment is pivotal in achieving homeownership success. By using the Mortgage Payment Calculator, you gain insights into various components such as interest rates, taxes, insurance, and PMI, which shape your monthly payments. This straightforward tool empowers you with accurate estimations, aiding in informed decision-making, whether you're a first-time homebuyer or considering refinancing. Leverage this tool to navigate the complexities of home financing with confidence, ensuring that your dream home fits well within your financial plans. Begin exploring your options today with clarity and assurance.